Betascore

Designing the solution where credit and financial data finally works for the credit invisibles

- Role

- UX Designer and PM

- Duration

- 6 months

- Team

- 1 UX designer1 Product manager3 Software Engineers1 Data Engineer

- My contributions

- ResearchStrategyLed end-to-end designTesting

Designing the gap between migrating and belonging financially

When people move to a new country, their credit history doesn't follow them. They become invisible to the financial system — unable to access credit, loans, or basic financial services regardless of their history back home. I was brought in as sole designer and product manager to solve that, designing Ndewo by BetaScore end-to-end across, collaborating with a small engineering team of three to take it from discovery to delivery.

Early traction, real results

User growth

5,000 users and counting since launch

The product has grown to 5,000 users since going live. A strong signal that credit invisibles were actively looking for exactly this solution.

Revenue metrics

Over £100k revenue, exceeding target by 25%

The product surpassed its revenue target by 25% since launch. Proof that solving a real financial gap translates directly into commercial traction.

Grant metrics

Over £20k grant from Manchester Growth Company

Secured a grant from Manchester Growth Company to build out the credit worthiness API service. Validation from a leading regional growth programme.

Industry recognition

Received award for “One to Watch” at Tech Climbers

Ndewo was awarded for the “One to Watch” at Tech Climbers. Recognition that the product was making waves beyond its user base.

Invisible to the system, not by choice

When people migrate, their financial identity doesn't travel with them. Years of responsible credit behaviour in their home country becomes meaningless the moment they cross a border, leaving them locked out of basic financial services in their new home.

Why it is important

There are 184 million people living outside their country of nationality. For millions of them, financial exclusion isn't a minor inconvenience — it's a barrier to building a stable life. Businesses are also missing out, unable to serve a growing and underserved market due to a lack of accessible data.

Credit invisibility: Migrants' home credit history isn't recognised by financial systems in their new country.

Data gap: Businesses lack access to migrants' financial data, making it impossible to assess creditworthiness fairly.

Financial literacy: Many migrants don't understand how credit works in their new country or how to build it from scratch.

Understanding the problem before solving it

I started with secondary research to understand the scale of the problem, then went directly to the people affected. Speaking with 15 migrants gave me the firsthand context that data alone couldn't provide.

Secondary research

Studied white papers from Experian, Forbes, and the World Bank to understand the global scale of credit invisibility and its impact on both migrants and financial institutions.

Primary research

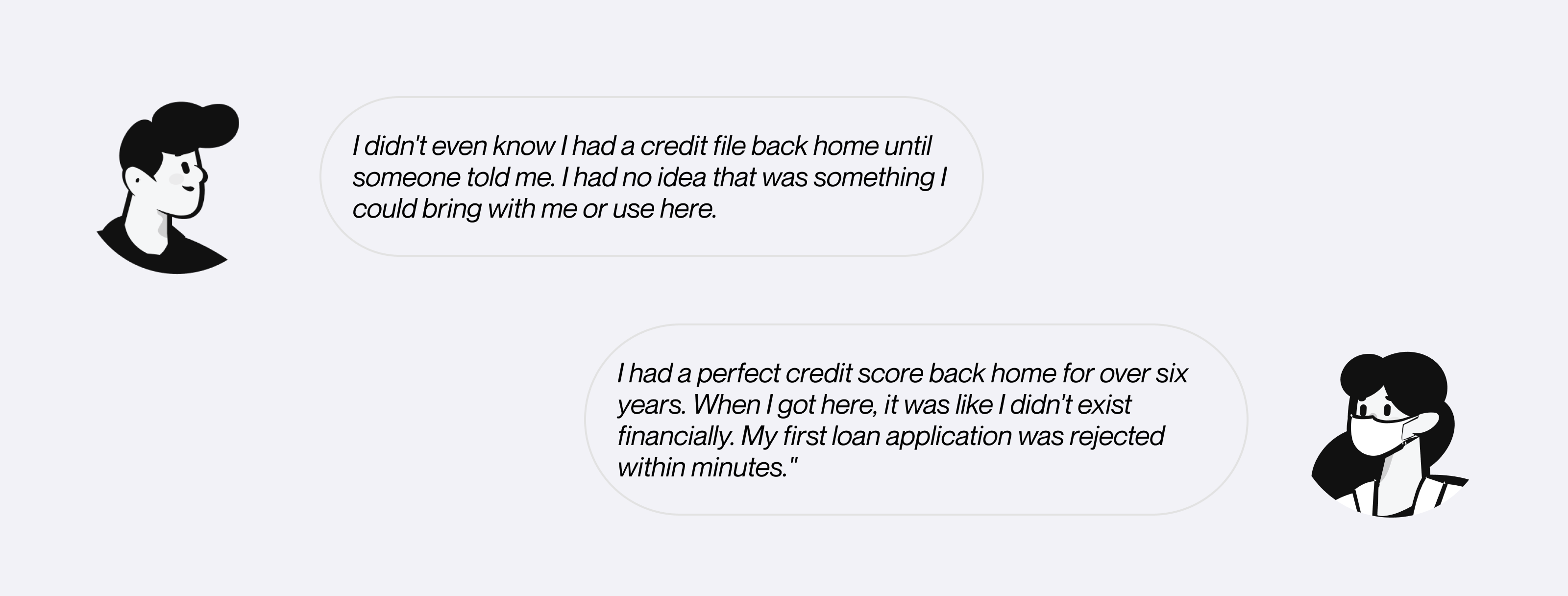

Spoke with 15 migrants directly to understand their lived experience — how they navigated financial systems, what they struggled with, and what they needed most.

Unaware of their own credit: 65% of participants didn't know their home country credit history existed or what made up a credit file.

Immediate but blocked: 30% tried to apply for credit cards or loans as soon as they arrived — and hit a wall.

No financial visibility: 40% didn't track their finances and had no insight into their spending habits.

The lens I designed through

Empowerment through education. Users needed to understand credit before they could act on it — knowledge had to come before access.

Localised insights, global solutions. Home country data had to be made meaningful in a new financial context, not just displayed.

Transparency and trust. Handling sensitive financial data meant being clear about what we were doing with it and why.

Seamless data integration. Raw credit bureau and bank data had to feel simple and human, regardless of how complex it was underneath.

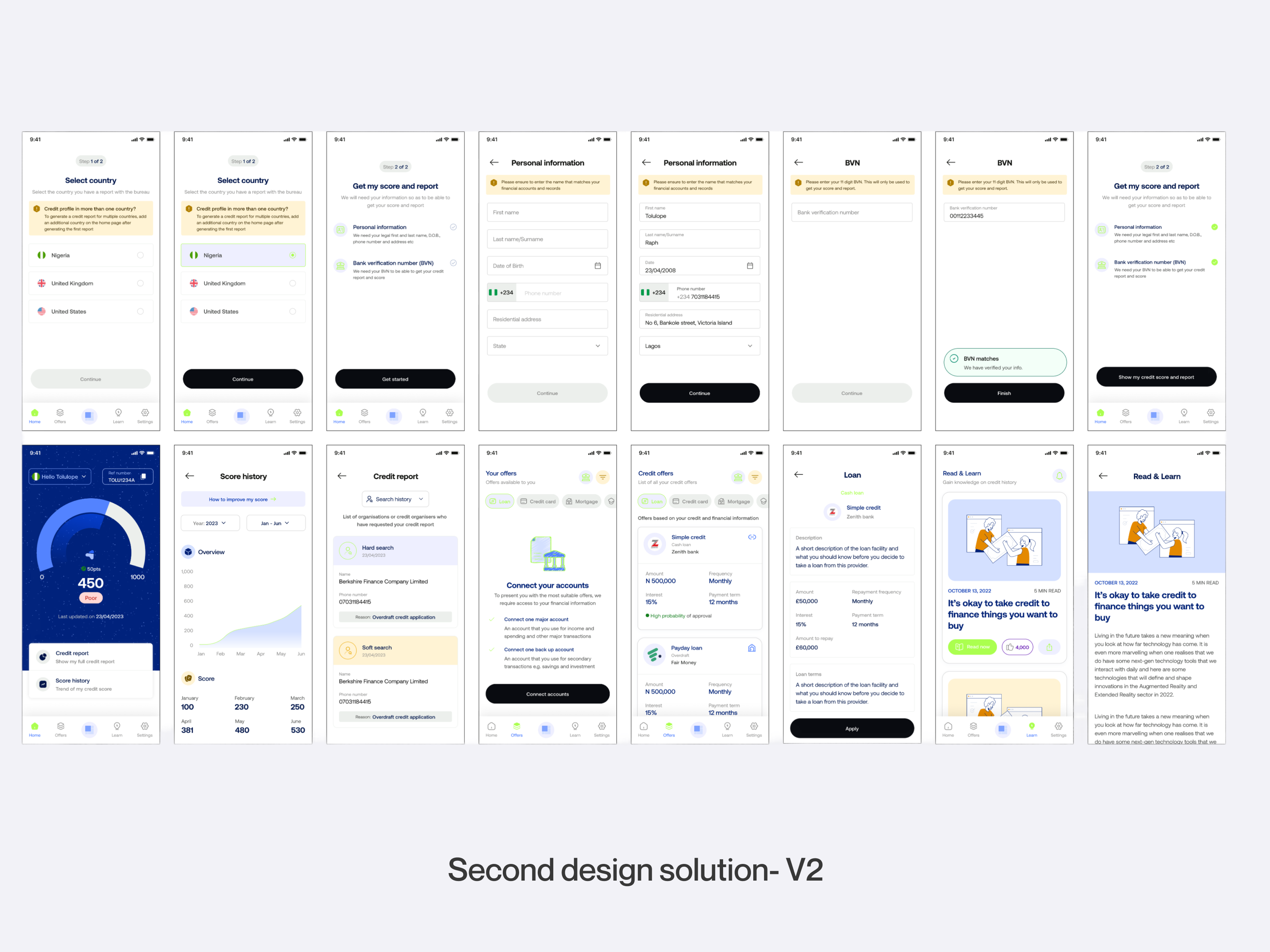

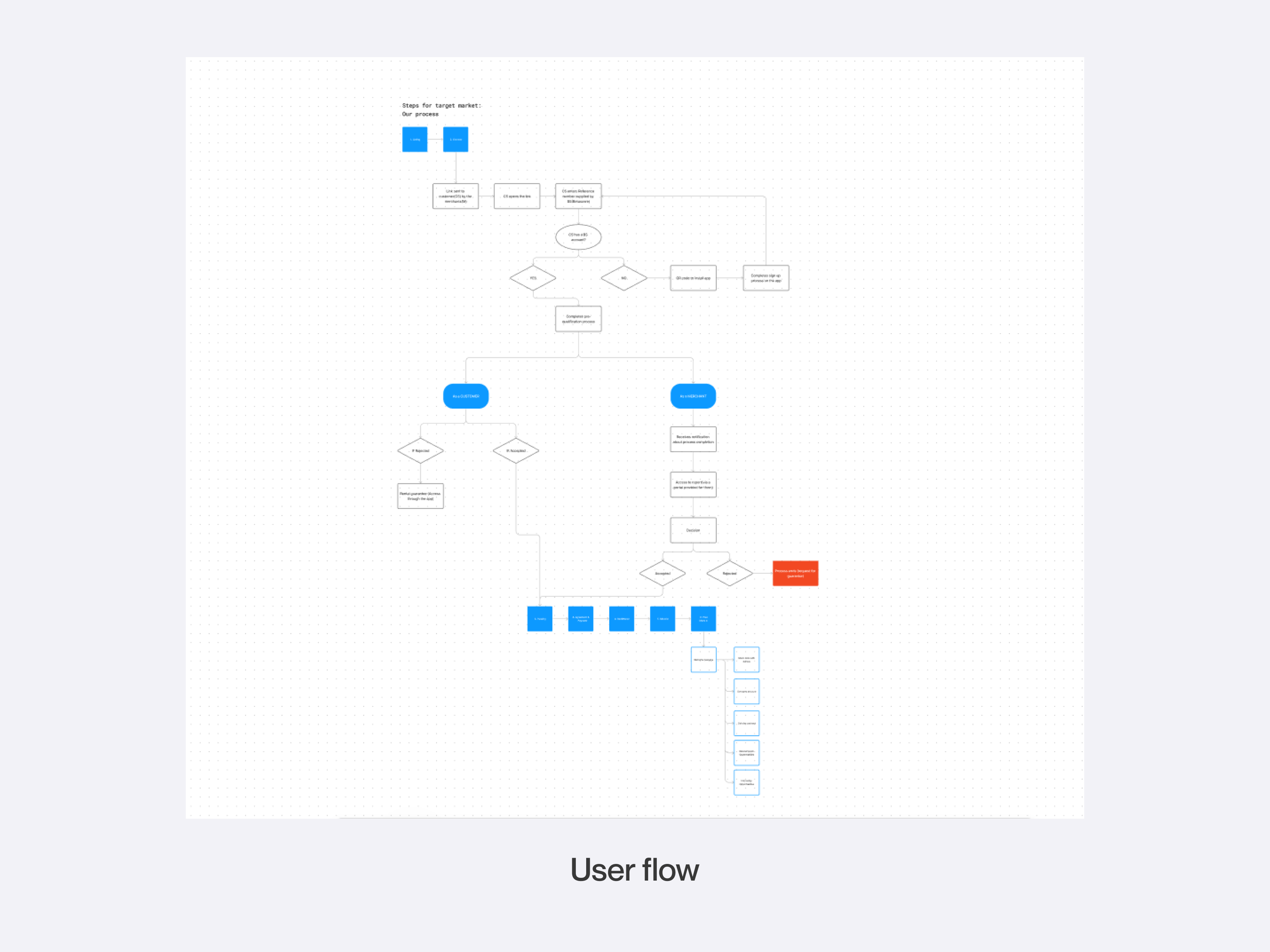

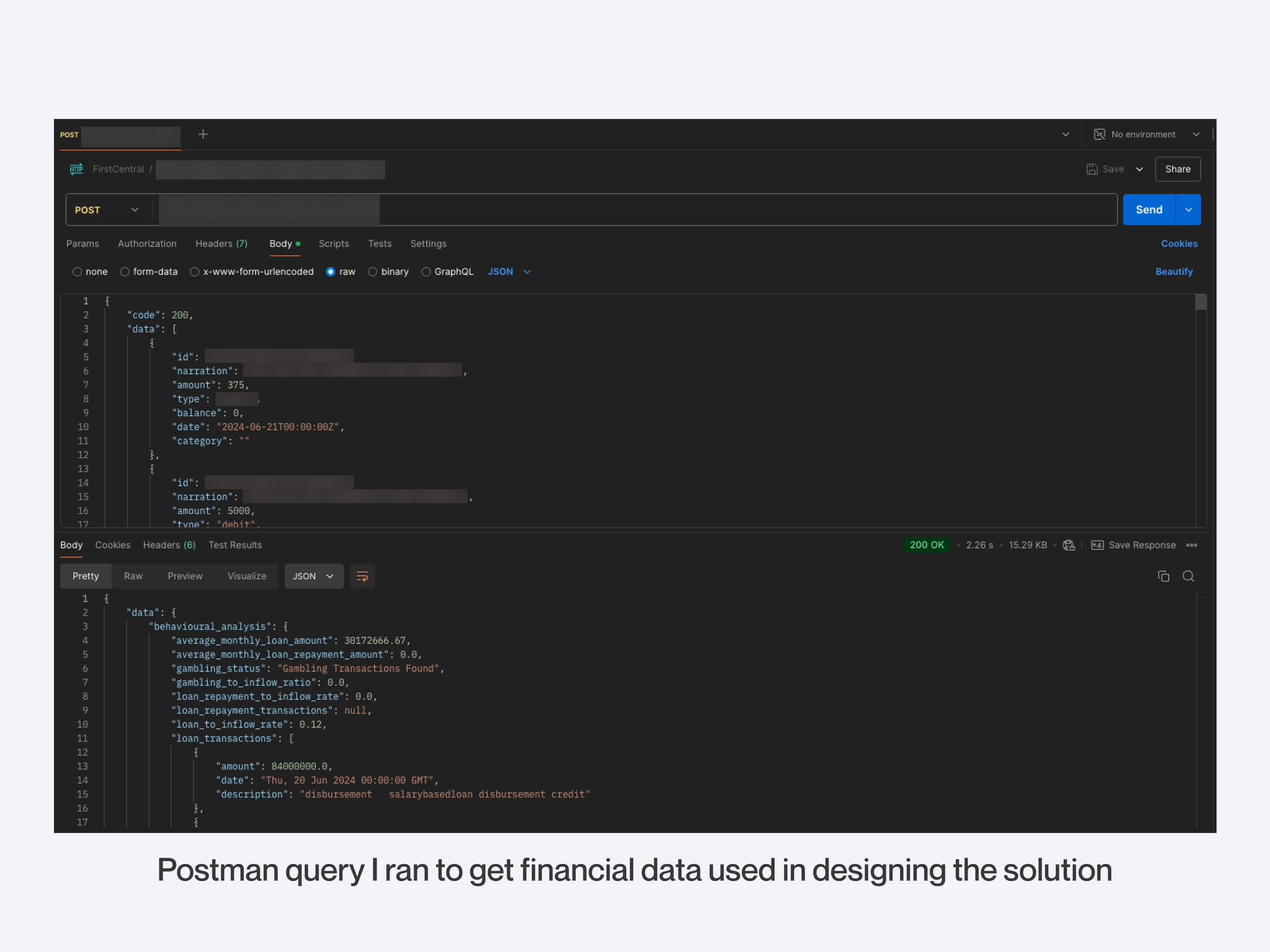

Turning invisible data into financial access

The biggest technical challenge was working with raw data from credit bureaus, banks, and internally created algorithms. To reduce reliance on developers, I taught myself to run POST, PUT and GET requests in Postman and read JSON files in VSCode — allowing me to explore the data independently and design interfaces that made complex data feel human.

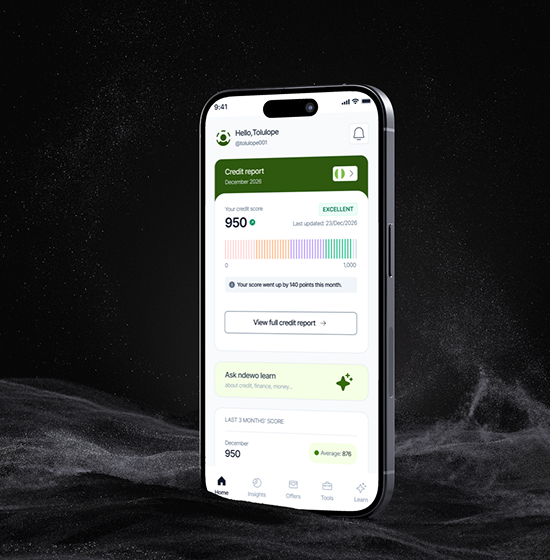

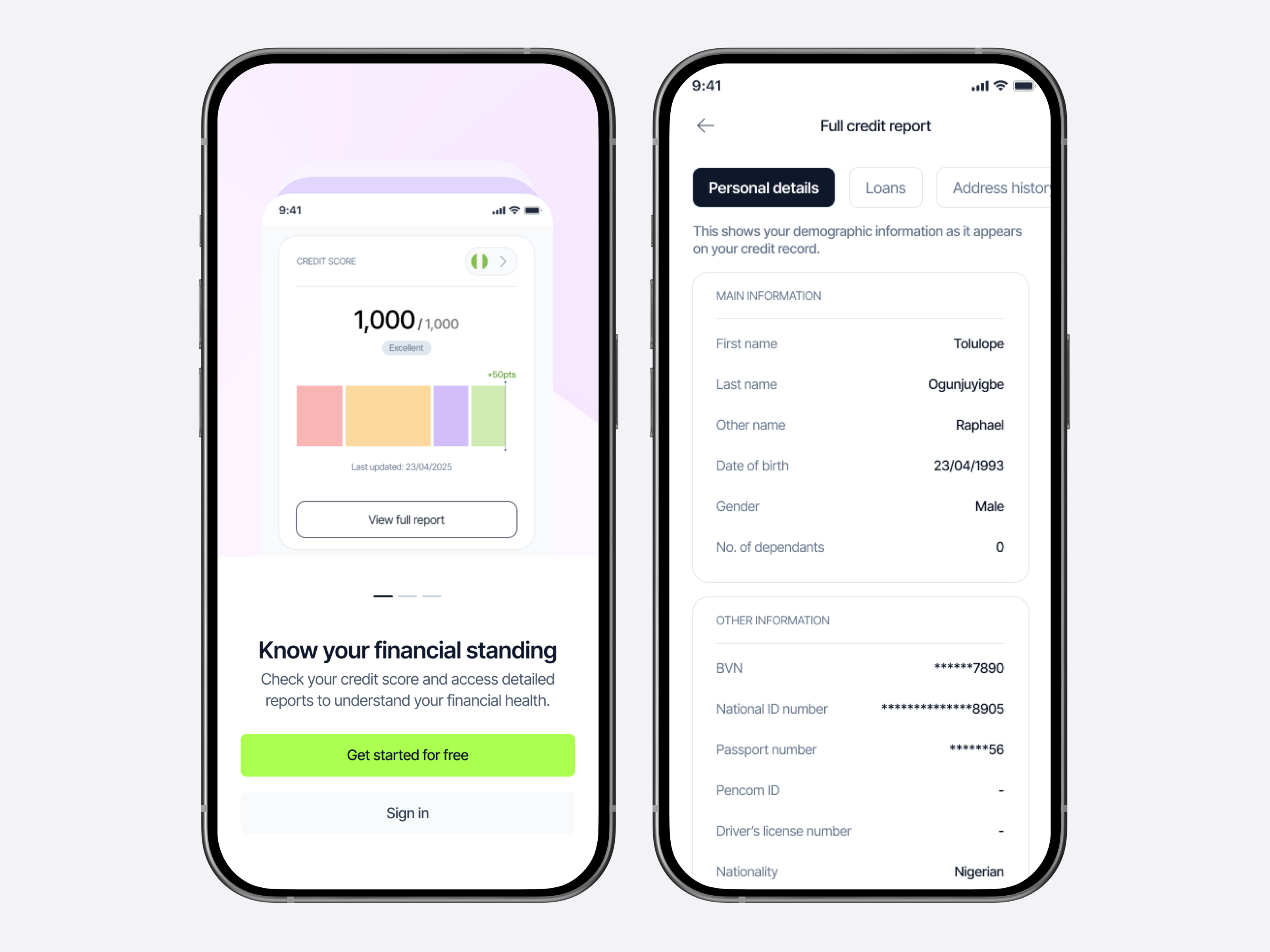

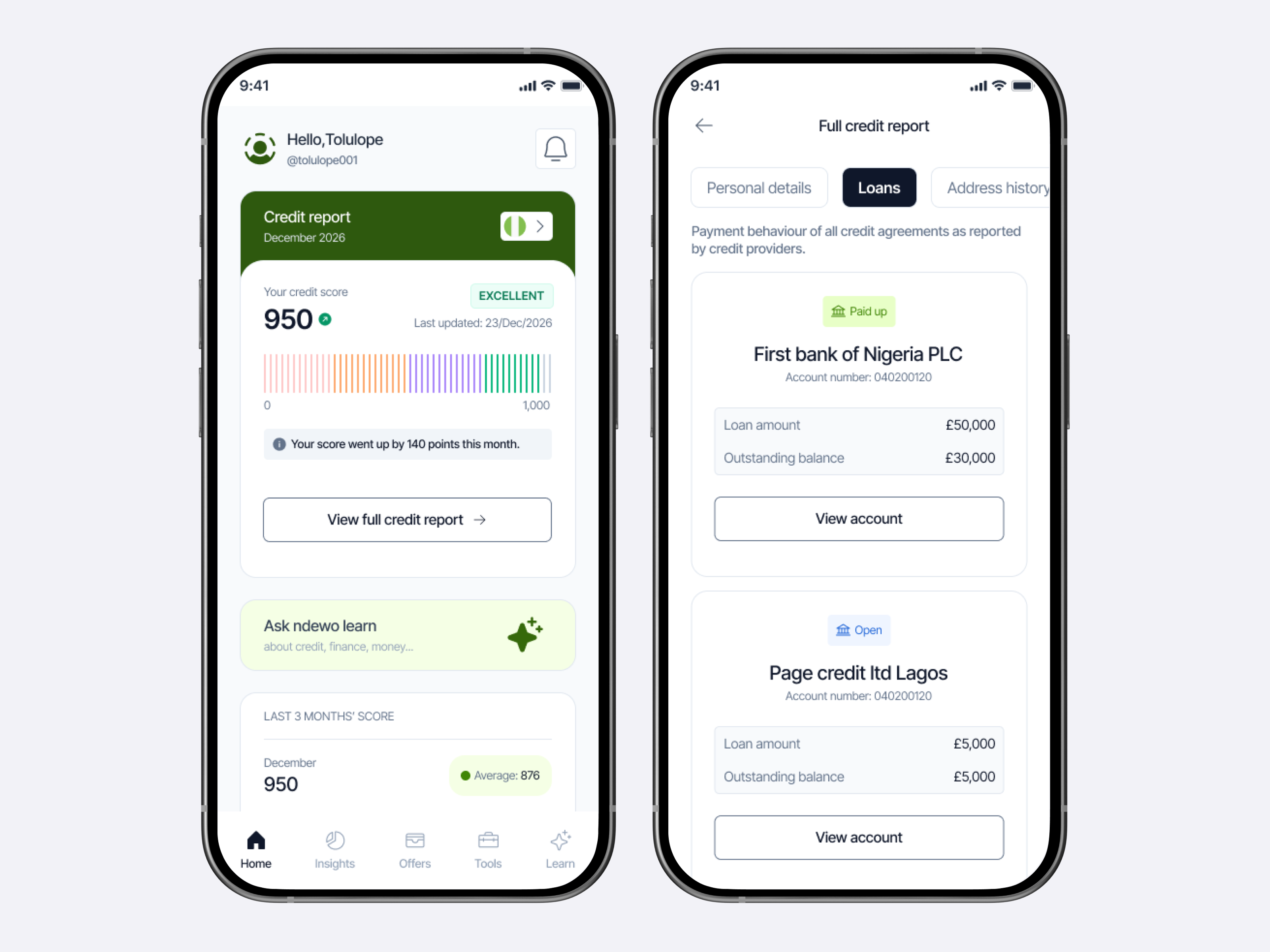

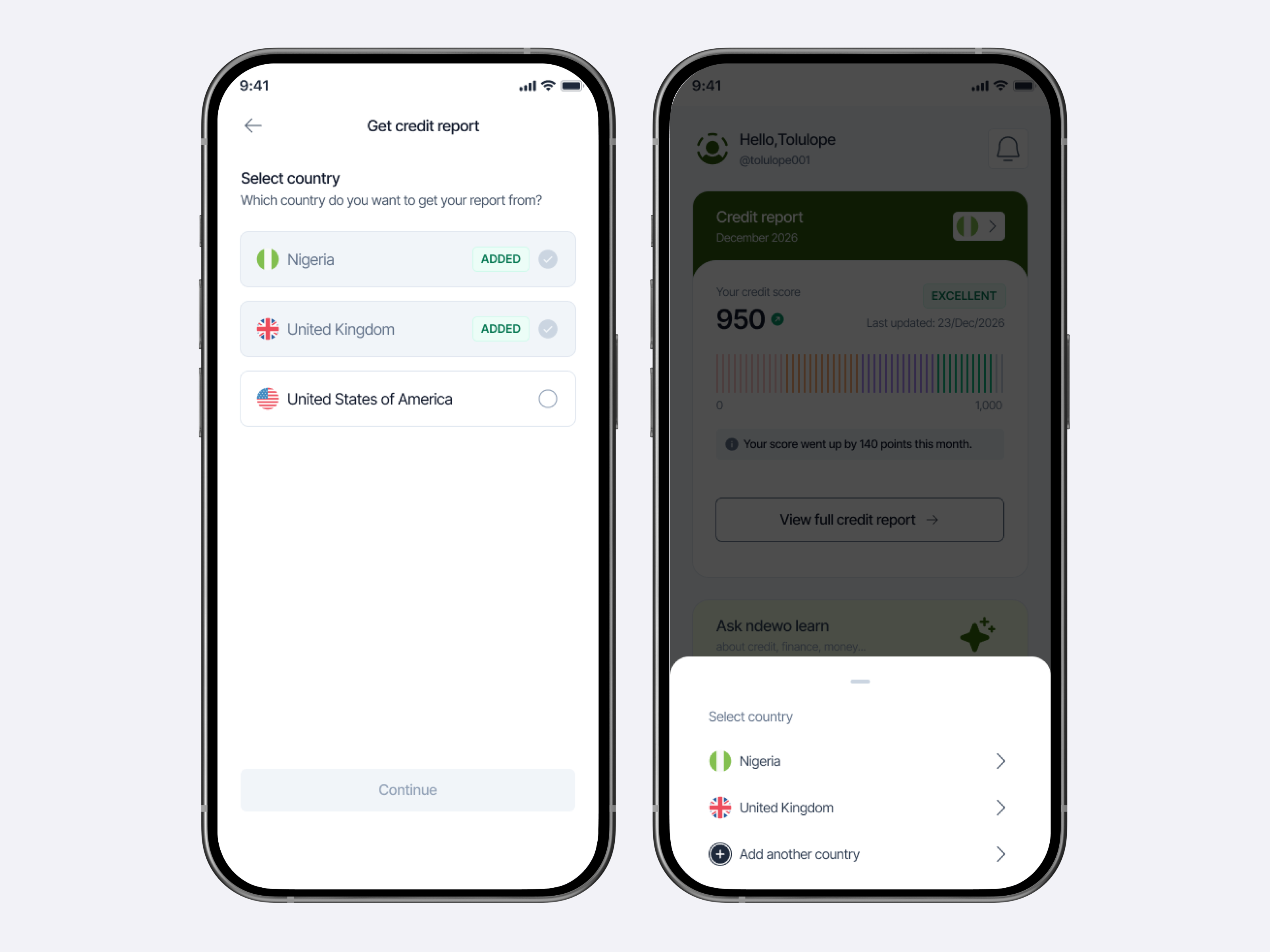

Report

Pulls credit history from the user's home country via the credit bureau in JSON format, organises it into meaningful categories, and presents it with detailed explanations. Users couldn't act on data they couldn't see or understand. Making home credit visible was the foundation of everything else.

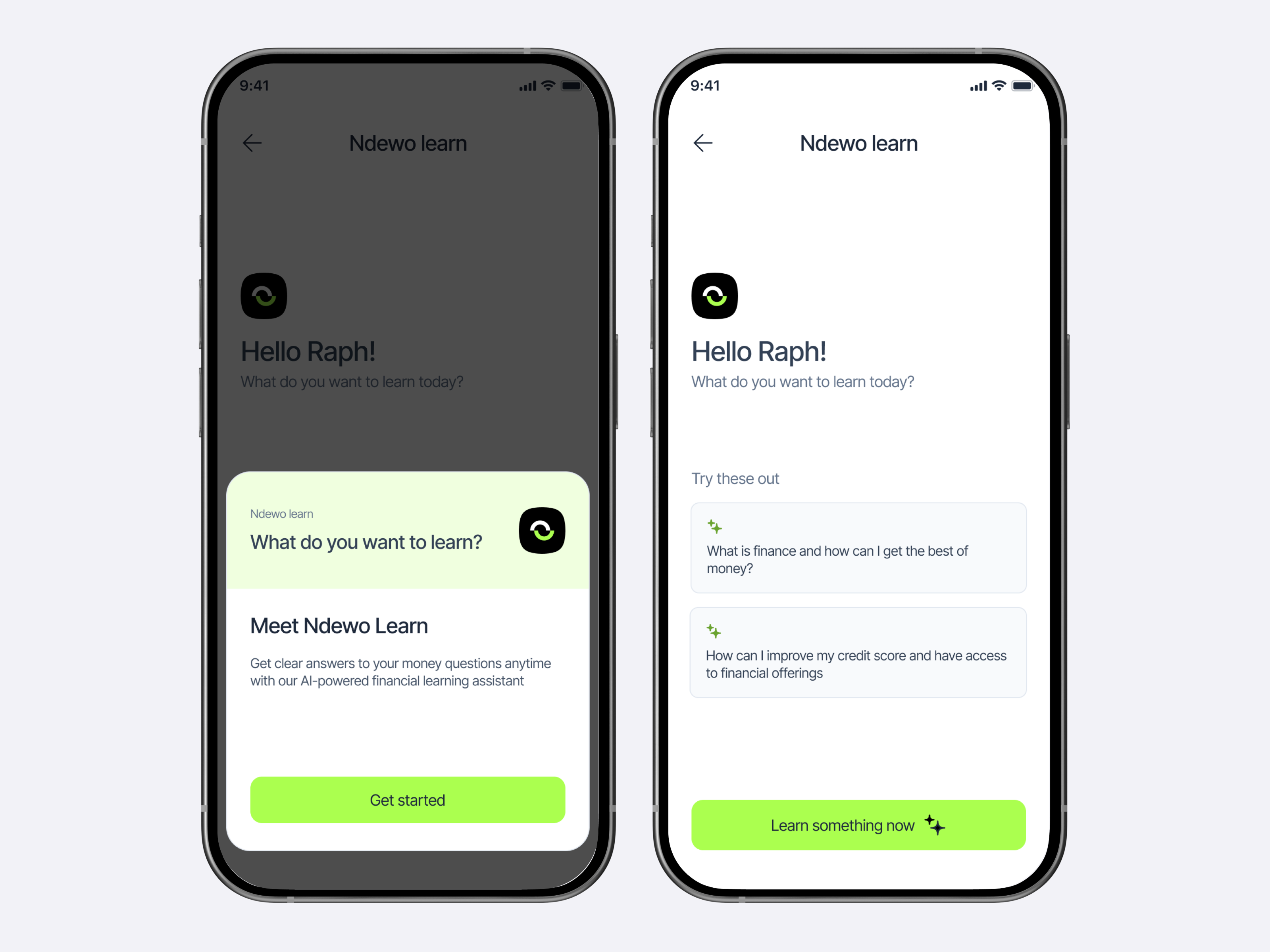

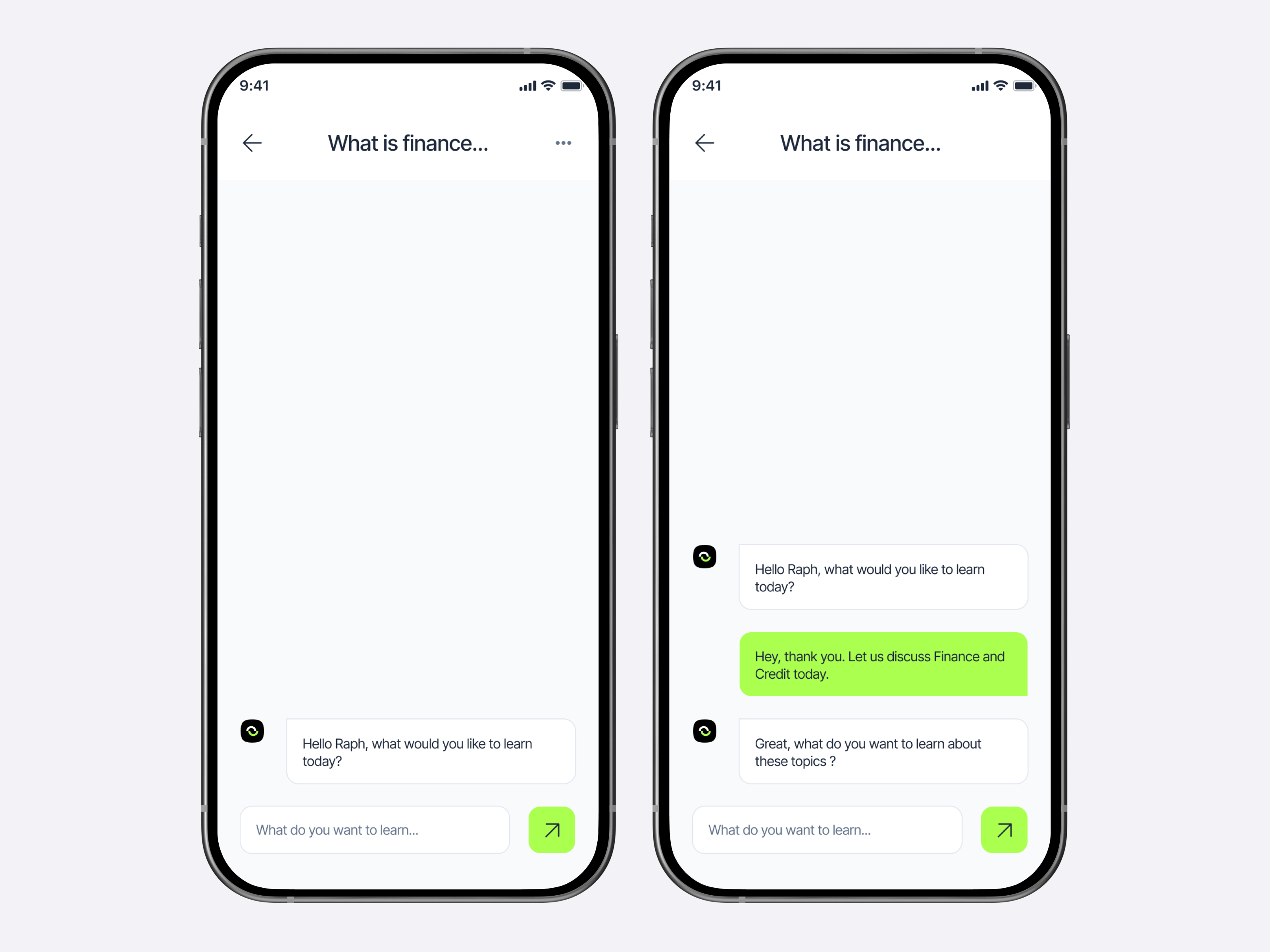

Learn

An AI-powered financial education feature modelled on a familiar chat interface, helping users understand credit and finance in their new country. 65% of users didn't understand credit. Education had to come before access.

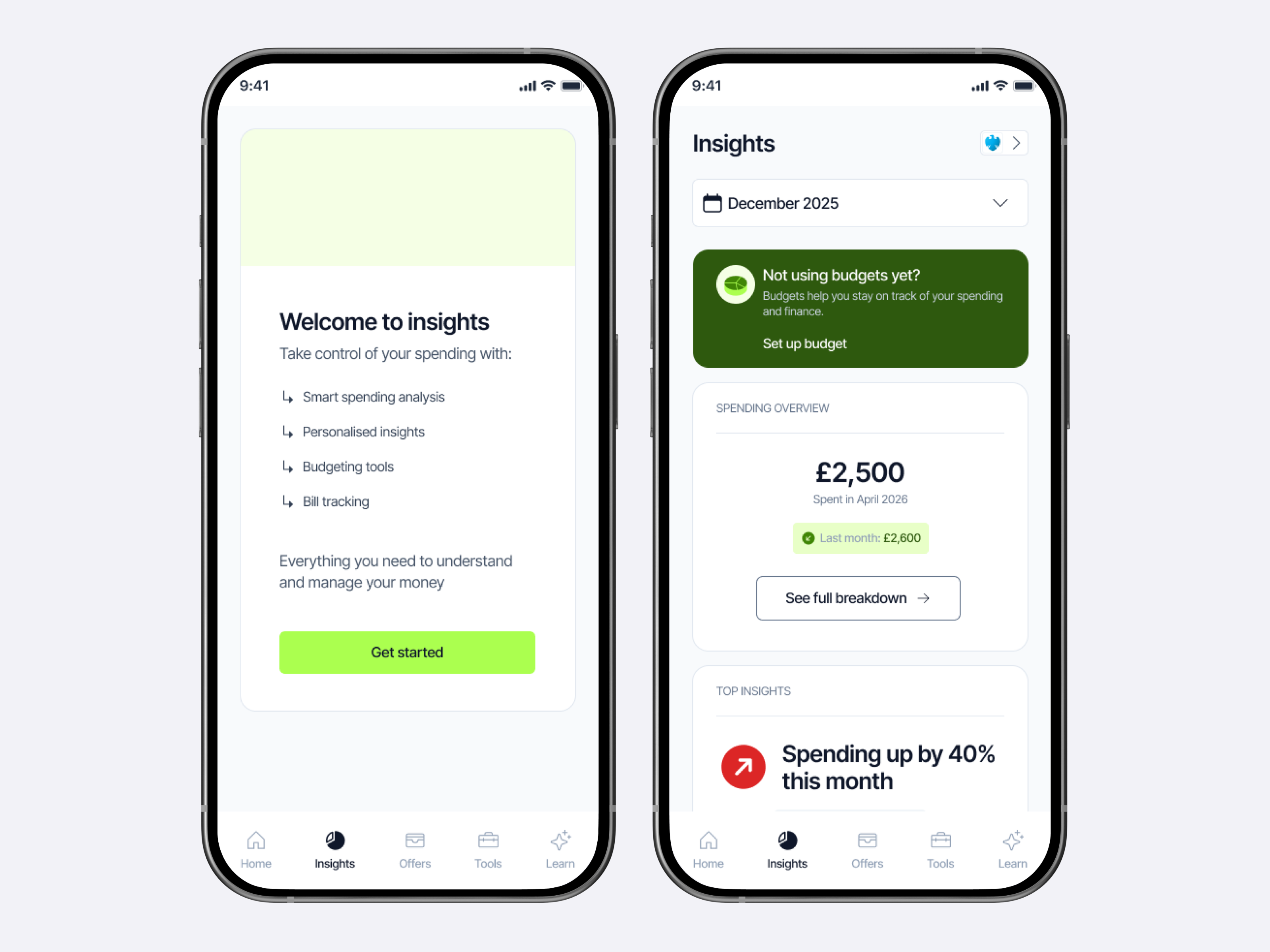

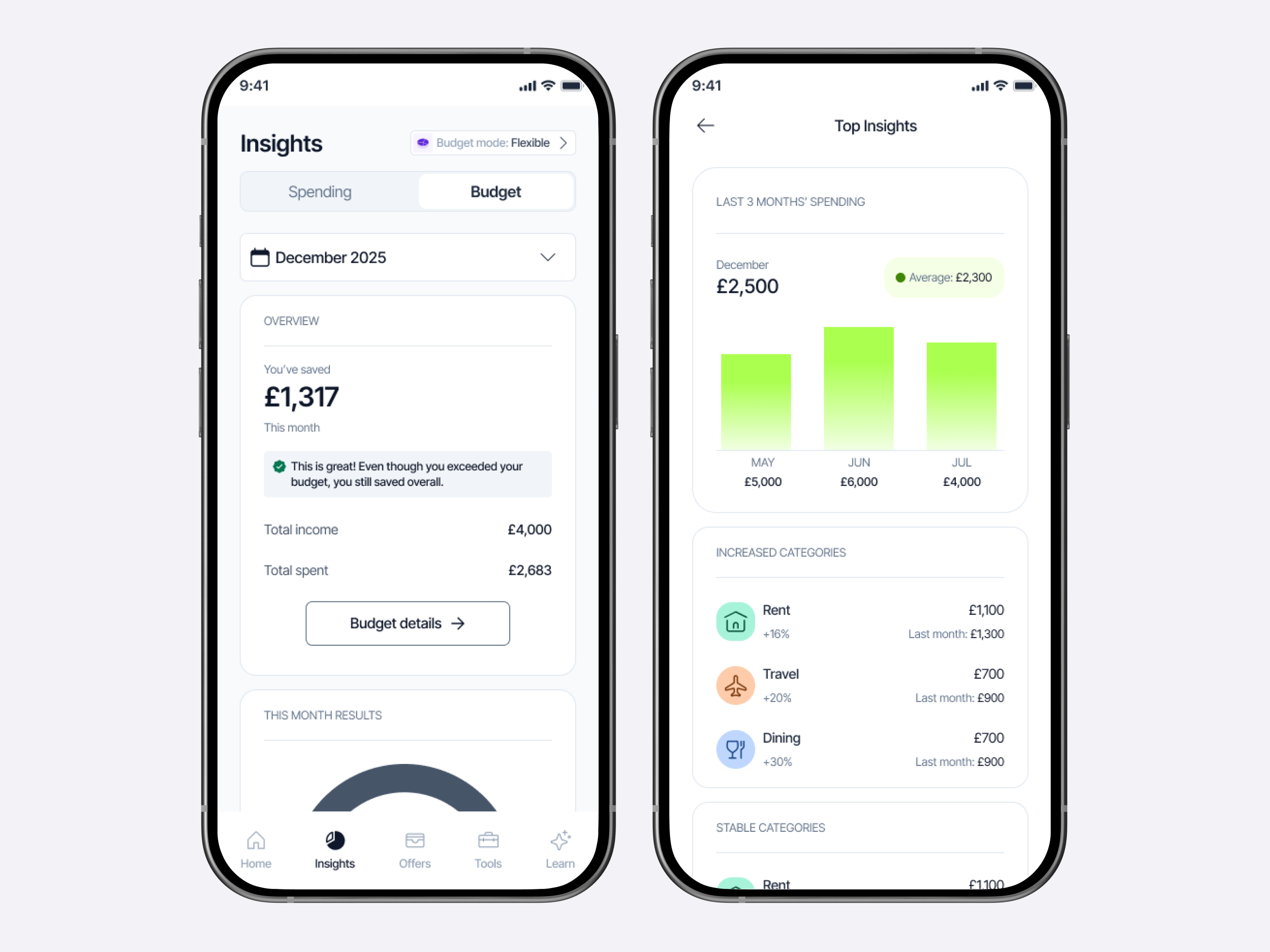

Insights

Extracts data from bank statements to generate a cash flow analysis, spending overview and category breakdowns. Understanding spending habits directly impacts credit access — users needed visibility into both.

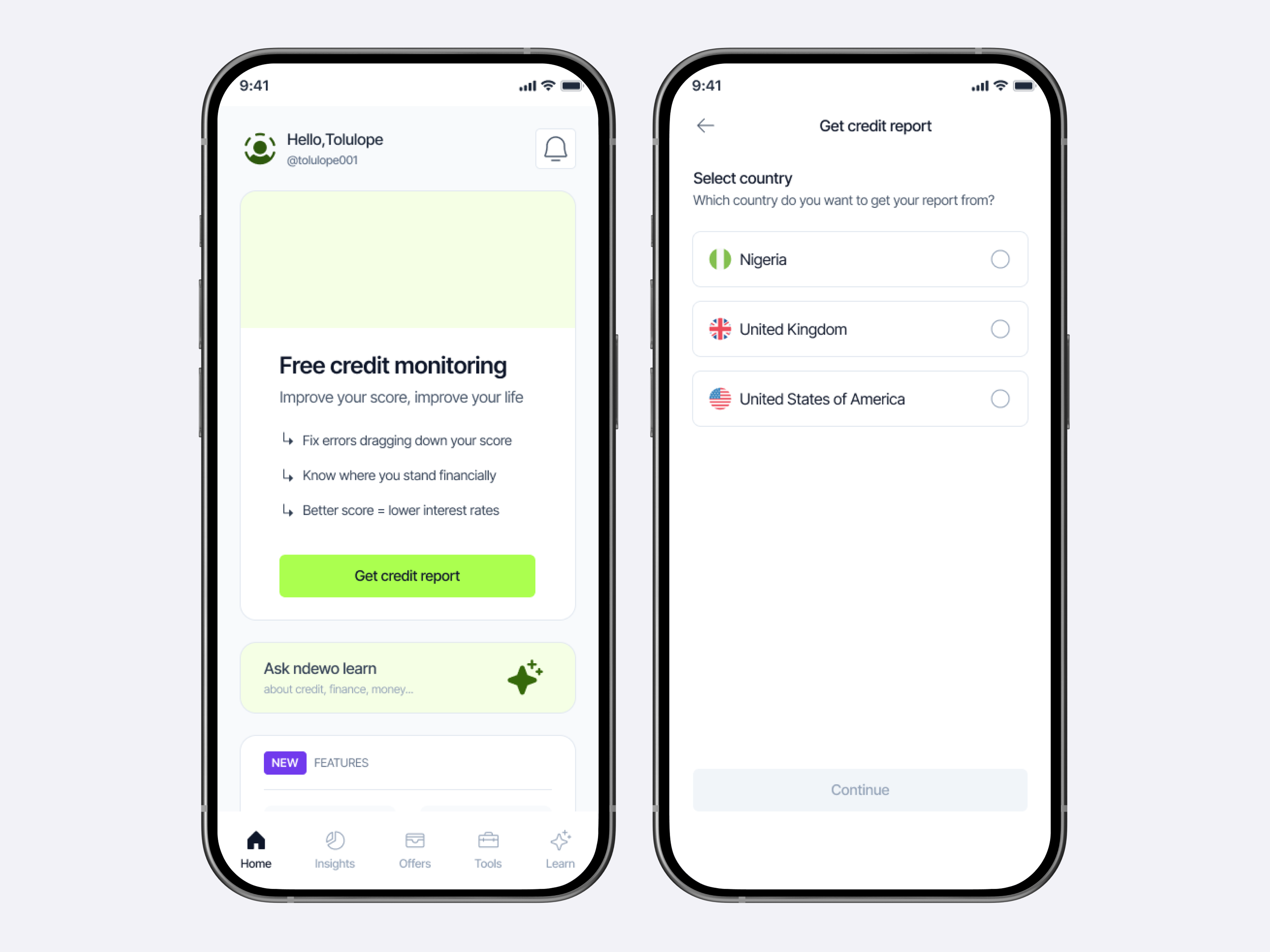

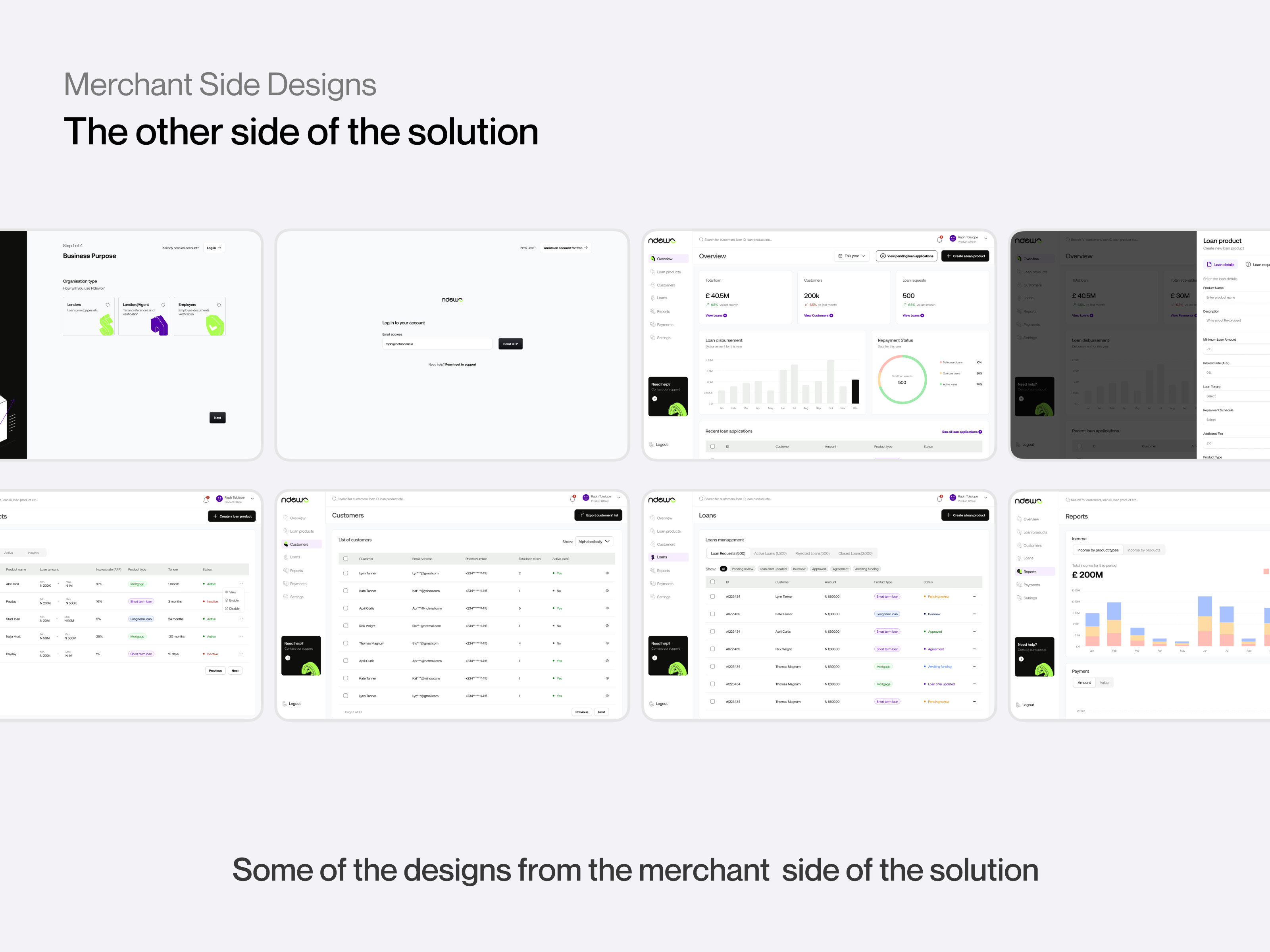

Merge

Merges credit histories from the user's previous and current country, which is then shared with businesses for credit decisions. This was the core unlock — turning invisible financial history into a recognised, actionable asset.

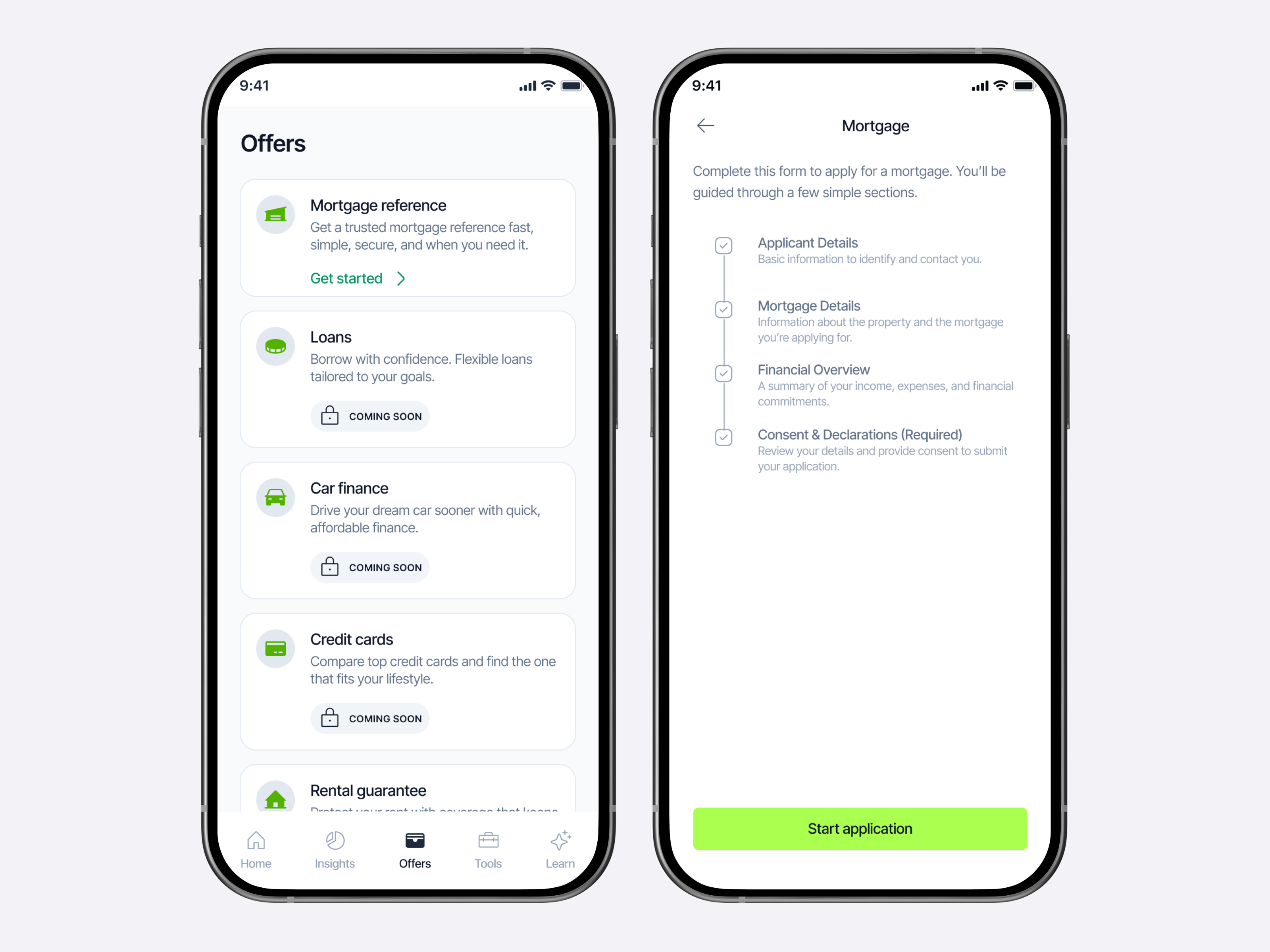

Offers

Users can access credit cards, loans, car finance and more from pre-permissioned providers. The entire product builds toward this moment — turning a score into real financial opportunity.

Shaped by people who used it

Identity security concerns

Users raised concerns about identity theft when connecting their financial data. Added clearer security messaging, data handling explanations, and additional verification steps throughout the flow. Trust is non-negotiable when handling sensitive financial data. Users needed to feel protected before they would connect anything.

Colour accessibility

Testers found the colour usage too heavy throughout the app for the initial versions. Scaled back the palette to create a cleaner, more accessible experience. A product built for inclusivity had to feel inclusive — visual overload was getting in the way of the content.

Financial data depth

Users wanted more detail in the financial data sections. Expanded the insights feature with richer breakdowns, spending categories, and clearer financial health indicators. The product's value is in the data — if users couldn't get enough from it, the core promise fell flat.

Beyond the case study

A selection of artefacts that didn't make the main story but were equally important in shaping the overall experience.

Lessons from the deep end

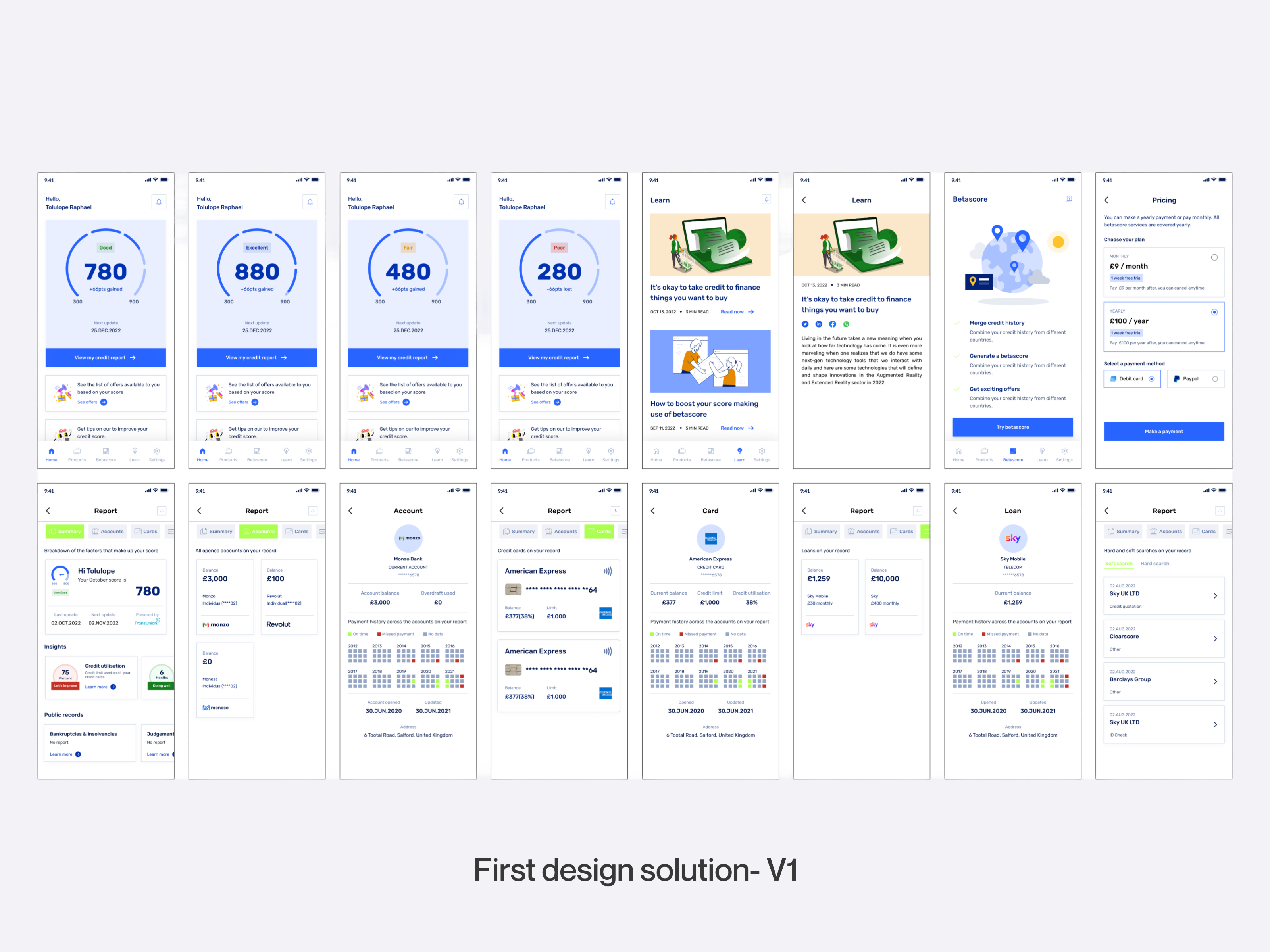

Ndewo was the project that pushed me furthest outside my comfort zone. Working with raw credit bureau data, learning Postman and JSON independently, and managing both design and product — it demanded more than just good design thinking. It taught me what it means to truly own a problem.

Learn the tools your engineers use.

Understanding Postman and JSON reduced my dependency on developers and made me a sharper, faster designer.

Complex data needs simple design.

The harder the data, the more important clarity becomes. Every screen had to translate complexity into something a first-time user could act on.

Owning the product changes how you design.

Being sole designer and PM meant every decision had commercial weight. It made me more deliberate, more strategic, and more accountable.